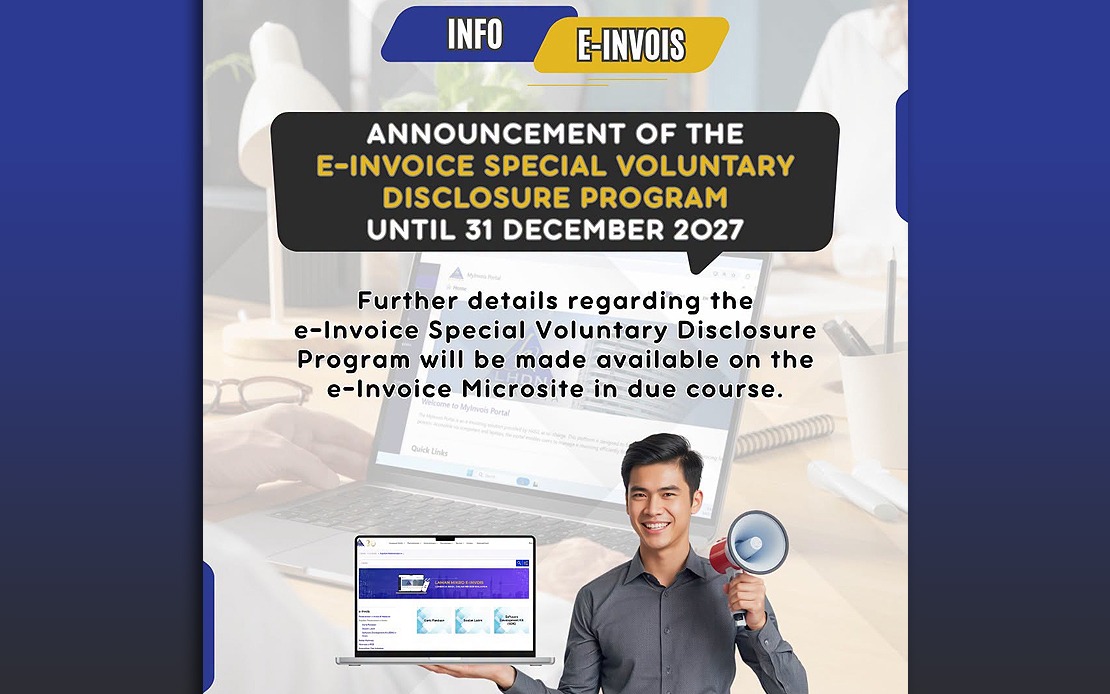

The Inland Revenue Board (IRB) has unveiled a sweeping amnesty programme that gives Malaysian businesses nearly three years to rectify their electronic invoicing records without financial penalty. The e-Invoice Special Voluntary Disclosure Programme (PKPS), running until December 31, 2027, represents a significant shift in the tax authority's approach to digital compliance, signalling an acknowledgment that the transition to mandatory e-invoicing has created genuine difficulties for Malaysia's business community, particularly smaller operators struggling with the technical and administrative demands.

Prime Minister Datuk Seri Anwar Ibrahim, who doubles as Finance Minister, framed the initiative as a deliberate policy choice to reduce the burden on micro, small, and medium enterprises (MSMEs) as they navigate the evolving digital economy. The announcement underscores the government's recognition that compliance penalties, while traditionally used to encourage adherence to tax rules, can sometimes prove counterproductive when businesses face systemic challenges in implementation. By removing the threat of financial consequences during this extended window, the IRB is attempting to foster voluntary cooperation and encourage businesses to bring their records into proper order.

Three distinct categories of taxpayers can benefit from the programme's protections. The first group comprises businesses that failed entirely to submit electronic invoices for specific qualifying transactions, a scenario that likely affected numerous sole proprietors and small operators who may have overlooked certain transactions or operated systems that weren't fully integrated with the e-invoicing infrastructure. The second category covers those who did submit invoices but with substantive errors or technical deficiencies that breached the stipulated requirements, a common problem when businesses rushed to adopt new systems without adequate training or support. The third and arguably broadest category extends protection to any taxpayer who missed submission deadlines for any period dating back to when e-Invoice implementation became compulsory.

The voluntary disclosure mechanism demands that participating businesses ensure their submissions are both accurate and fully compliant with the IRB's General and Specific e-Invoice Guidelines. This requirement reflects a balance between leniency and responsibility—while penalties are waived, the underlying obligation to provide correct information remains non-negotiable. Businesses cannot use the amnesty as cover for intentional misrepresentation; rather, it functions as a correction and regularisation tool for those who acted in good faith or faced genuine implementation obstacles.

Beyond the penalty waiver, the government has sweetened the offer by accelerating tax incentives for compliant taxpayers. A particularly valuable provision allows businesses to claim capital allowances for information and communication technology (ICT) equipment purchases and software development costs entirely within a single fiscal year. Traditionally, such expenses would be depreciated across multiple years, meaning companies investing heavily in systems to support e-invoicing compliance can now recover those costs much faster, effectively reducing their taxable income in the year the investment occurs. This financial incentive directly addresses one of the primary concerns for MSMEs—the upfront cost of digital infrastructure.

The timing of this initiative reflects broader economic considerations within Malaysia's fiscal environment. As the country seeks to modernise its tax administration and create a more digitalised economy, the government faces a political imperative to avoid creating excessive friction that might discourage business formation or drive enterprises toward informal sectors. The PKPS represents a pragmatic acknowledgment that top-down compliance mandates, without adequate adjustment periods and support mechanisms, can generate resentment and non-compliance, particularly among businesses lacking sophisticated accounting departments.

For Malaysian MSMEs and small business owners, the programme offers tangible relief. Many have struggled with the complexity of integrated e-invoicing systems, particularly those operating in traditional sectors like retail, hospitality, and services where digital infrastructure may be less developed. The IRB's provision of multiple support channels—including dedicated helpdesks, Live Chat services, and nationwide office consultations—suggests an intent to make the compliance process more navigable going forward. The decision to establish specific e-Invoice helpline infrastructure at 03-8682 8000 indicates the tax authority anticipated questions and challenges from the business community.

The broader regional context matters here. Southeast Asian economies are pursuing varying approaches to digital tax administration, and Malaysia's relatively generous amnesty programme may influence how neighbouring countries balance digital modernisation against business compliance costs. Singapore, Thailand, and Indonesia are all grappling with similar e-invoicing transitions, and Malaysia's inclusive approach could establish a regional benchmark for balancing revenue administration with business support.

However, the programme's success depends critically on awareness and outreach. Many small business owners may remain unaware of the amnesty's existence or the specific deadlines and procedures for participation. The IRB will need to undertake substantial communication campaigns in English, Malay, Mandarin, and Tamil to ensure that businesses in different communities understand the opportunity available to them. Without effective messaging, even a generous compliance programme risks failing to achieve its intended impact.

The December 31, 2027 deadline effectively provides businesses with a two-and-a-half-year runway to resolve their e-Invoice compliance issues. This extended timeline suggests the government believes that most outstanding issues can be remedied within this period if businesses commit resources and effort. For those who fail to regularise their position before the deadline, however, the IRB will presumably return to standard enforcement procedures, making the date a genuine cutoff rather than a suggestion.

Looking forward, this programme signals the government's broader philosophy on digital transformation policy. Rather than imposing strict penalties from the outset, Malaysia is attempting to incentivise voluntary compliance through a combination of penalty waivers and financial sweeteners. This carrot-and-stick approach, where the stick remains implicit rather than immediately wielded, reflects contemporary thinking about regulatory design in digital economies where technology adoption requires genuine business participation and buy-in.